Management Accounting Answers Test Synergy

Content: Ответы на тест.zip (119.63 KB)

Uploaded: 16.12.2020

Positive responses: 0

Negative responses: 0

Sold: 7

Refunds: 0

$1.99

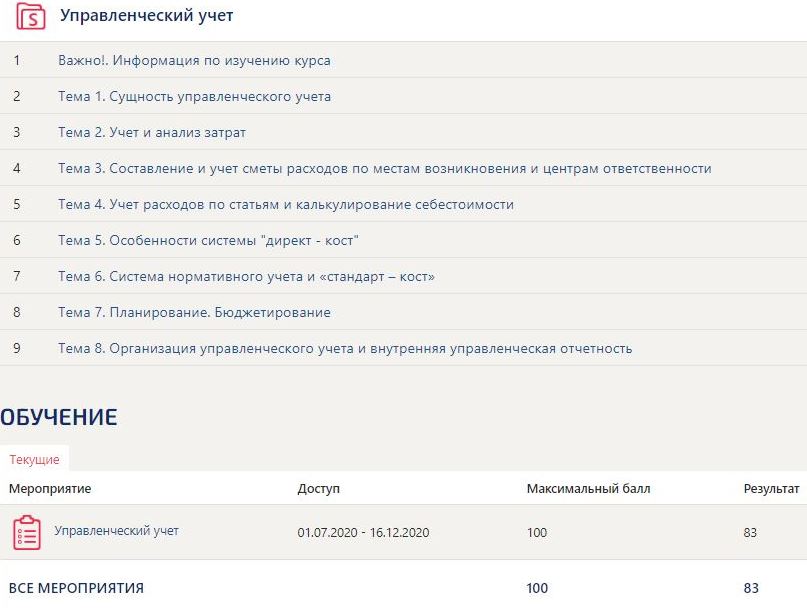

Management accounting answers to Synergy tests. Score 83 points

With this method of calculating the cost of production as Direct-costing, the cost of production includes:

all direct costs of production;

all variable costs of production;

all variable costs of production, excluding selling and administrative expenses.

Transactions covering the financial activities of the enterprise are reflected:

in the operating budget;

in the financial budget.

Which of the following methods of calculating the cost of production will have the lowest profit on the sale of products:

when calculating the full cost of production;

when calculating the production cost of products;

when calculating the cost of production using the Direct-Costing method.

Direct costs of manufacturing products include:

equipment maintenance and operation costs;

cost of basic materials;

equipment adjuster wages;

wages of key production workers.

The accounting sources of information used in management accounting include:

intradepartmental audit materials;

accounting data;

printing materials;

materials obtained in the course of personal contacts with performers;

operational and statistical data;

explanatory and memorandums.

Calculation objects are:

internal pricing;

production costs;

income from ordinary activities.

Costs are classified according to the way they are included in the cost of production:

main and overhead

direct and indirect

variables and constants

General production costs are:

general running costs

equipment maintenance and operation costs

general shop management costs

The main costs associated with the production of products include the following types of costs:

depreciation of an administrative building;

the cost of semi-finished products used to manufacture products;

communal payments;

the salary of the management personnel of the organization;

wages of key production workers.

Is it possible to use the Direct-Costing method for drawing up external reporting of an enterprise:

Yes;

no.

Management accounting uses the following methods:

accounts and double entry;

index method;

least squares methods.

all answer options

When budgeting, the center of responsibility means:

any production site of the enterprise;

the head of a division or department;

segment of the enterprise, for the results of which its manager is responsible.

The cost accounting object for the per-turn costing method is:

order;

contract;

type of products manufactured;

a set of technological operations (stage of the production process);

costs of the production process as a whole.

Examples of single-element costs are the following costs:

general running costs;

business expenses;

the cost of basic materials for the production of products;

equipment repair costs.

Costs are grouped by centers of origin in management accounting:

by types of products (works, services) intended for sale;

by production units;

by economic elements.

Specific fixed costs:

change depending on the business activity of the organization;

remain practically unchanged over a period of time;

do not depend on the business activity of the organization and always have a constant value.

A calculation based on the actual production costs incurred is called:

Actual;

estimated;

planned.

Management functions are:

forecasting;

analysis;

audit;

planning.

Costs are involved in calculating the margin profit:

permanent:

variables:

option or depending on the type of management decisions.

With this method of calculating the cost of production as Direct-costing, the cost of production includes:

all direct costs of production;

all variable costs of production;

all variable costs of production, excluding selling and administrative expenses.

Transactions covering the financial activities of the enterprise are reflected:

in the operating budget;

in the financial budget.

Which of the following methods of calculating the cost of production will have the lowest profit on the sale of products:

when calculating the full cost of production;

when calculating the production cost of products;

when calculating the cost of production using the Direct-Costing method.

Direct costs of manufacturing products include:

equipment maintenance and operation costs;

cost of basic materials;

equipment adjuster wages;

wages of key production workers.

The accounting sources of information used in management accounting include:

intradepartmental audit materials;

accounting data;

printing materials;

materials obtained in the course of personal contacts with performers;

operational and statistical data;

explanatory and memorandums.

Calculation objects are:

internal pricing;

production costs;

income from ordinary activities.

Costs are classified according to the way they are included in the cost of production:

main and overhead

direct and indirect

variables and constants

General production costs are:

general running costs

equipment maintenance and operation costs

general shop management costs

The main costs associated with the production of products include the following types of costs:

depreciation of an administrative building;

the cost of semi-finished products used to manufacture products;

communal payments;

the salary of the management personnel of the organization;

wages of key production workers.

Is it possible to use the Direct-Costing method for drawing up external reporting of an enterprise:

Yes;

no.

Management accounting uses the following methods:

accounts and double entry;

index method;

least squares methods.

all answer options

When budgeting, the center of responsibility means:

any production site of the enterprise;

the head of a division or department;

segment of the enterprise, for the results of which its manager is responsible.

The cost accounting object for the per-turn costing method is:

order;

contract;

type of products manufactured;

a set of technological operations (stage of the production process);

costs of the production process as a whole.

Examples of single-element costs are the following costs:

general running costs;

business expenses;

the cost of basic materials for the production of products;

equipment repair costs.

Costs are grouped by centers of origin in management accounting:

by types of products (works, services) intended for sale;

by production units;

by economic elements.

Specific fixed costs:

change depending on the business activity of the organization;

remain practically unchanged over a period of time;

do not depend on the business activity of the organization and always have a constant value.

A calculation based on the actual production costs incurred is called:

Actual;

estimated;

planned.

Management functions are:

forecasting;

analysis;

audit;

planning.

Costs are involved in calculating the margin profit:

permanent:

variables:

option or depending on the type of management decisions.

The actual cost of goods produced for the reporting period is determined by the formula:

Debit turnover on account 20 = Initial balance on account 20 + Credit turnover on account 20 - Final balance on account 20;

Credit turnover on account 20 = Initial balance on account 20 + Debit turnover on account 20 - Final balance on account 20;

Debit turnover on account 20 = Initial balance on account 20 - Credit turnover on account 20 + Final balance on account 20.

Overhead costs include costs recorded on the account:

20 "Main production";

25 "General production costs";

26 "General expenses";

Does the subject of management accounting relate to business transactions of a financial nature (transactions with securities, rental and leasing transactions, investments in other organizations):

yes, they do;

no, do not apply.

Organization of management accounting:

internal affair of each enterprise

regulated by the state

tax authority demand

decision of the company´s shareholders

The separation of management accounting from the unified accounting system is due to the requirements:

internal users of information within the enterprise

creditors

tax authorities

banks

The cost accounting object for the custom-made costing method is:

order;

contract;

type of products manufactured;

process technology;

production process costs.

Work in progress is the cost:

for purchase, storage, transportation

production resources that, due to technological features, have not been implemented at a certain point

production resources that, due to technological features, at a certain point did not turn into finished products

for the production and sale of finished products

The list of cost items is approved:

By the enterprise itself

according to PBU 10/99 "Organization costs"

by the state, but not mandatory

Ministry of Finance of the Russian Federation

Direct costs of manufacturing products include:

the wages of equipment adjusters who are on the time-based wage system;

the cost of the basic materials used to manufacture the product;

costs associated with the preparation and development of production;

depreciation of office premises on a straight-line basis.

wages of key production workers;

The calculation compiled for the planning period based on the current norms is called:

Actual;

estimated;

planned.

Materials are:

direct costs

indirect costs

fixed costs

variable costs

* After purchase, you will receive answers to the questions that are indicated in the product description

Debit turnover on account 20 = Initial balance on account 20 + Credit turnover on account 20 - Final balance on account 20;

Credit turnover on account 20 = Initial balance on account 20 + Debit turnover on account 20 - Final balance on account 20;

Debit turnover on account 20 = Initial balance on account 20 - Credit turnover on account 20 + Final balance on account 20.

Overhead costs include costs recorded on the account:

20 "Main production";

25 "General production costs";

26 "General expenses";

Does the subject of management accounting relate to business transactions of a financial nature (transactions with securities, rental and leasing transactions, investments in other organizations):

yes, they do;

no, do not apply.

Organization of management accounting:

internal affair of each enterprise

regulated by the state

tax authority demand

decision of the company´s shareholders

The separation of management accounting from the unified accounting system is due to the requirements:

internal users of information within the enterprise

creditors

tax authorities

banks

The cost accounting object for the custom-made costing method is:

order;

contract;

type of products manufactured;

process technology;

production process costs.

Work in progress is the cost:

for purchase, storage, transportation

production resources that, due to technological features, have not been implemented at a certain point

production resources that, due to technological features, at a certain point did not turn into finished products

for the production and sale of finished products

The list of cost items is approved:

By the enterprise itself

according to PBU 10/99 "Organization costs"

by the state, but not mandatory

Ministry of Finance of the Russian Federation

Direct costs of manufacturing products include:

the wages of equipment adjusters who are on the time-based wage system;

the cost of the basic materials used to manufacture the product;

costs associated with the preparation and development of production;

depreciation of office premises on a straight-line basis.

wages of key production workers;

The calculation compiled for the planning period based on the current norms is called:

Actual;

estimated;

planned.

Materials are:

direct costs

indirect costs

fixed costs

variable costs

* After purchase, you will receive answers to the questions that are indicated in the product description

No feedback yet